Calling the bottom, the European CRE cycle is turning!

The European CRE markets have bottomed. Cap rates have stabilised, and solid operating fundamentals have kept rents ticking up despite a slowdown in the economy. CRE market indices and REIT indices have already begun to rebound, some big deals are hitting the headlines and transaction flows are picking up, and it seems highly likely that a new cycle is starting.

Chart 1 – CRE Prices

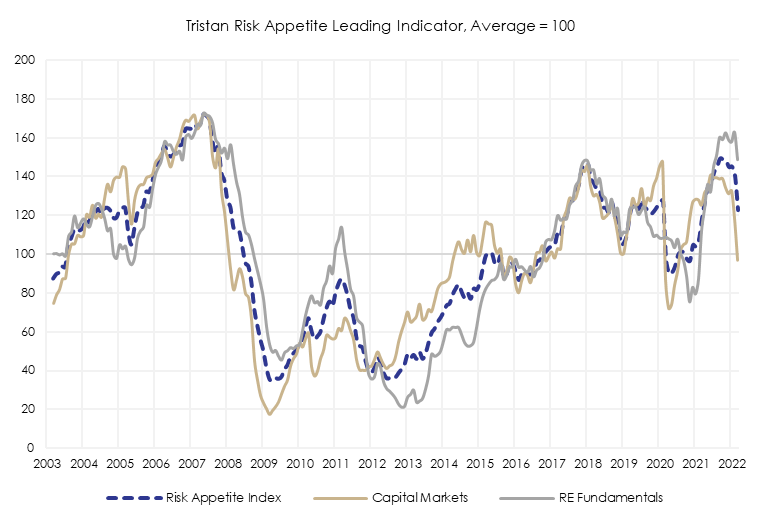

This is no great surprise. After a big correction in response to rates spiking dramatically in 2022 and a near complete cessation of deal activity, the prospect of rates being cut and curve normalisation was always likely to be a catalyst for flows. The turning point is now clearly visible in the key leading indicators, which have been ticking up now since the first quarter of 2024.

Chart 2 – European CRE Sentiment Indicator (INREV)

The European CRE market opportunity is significant!

In practice, turning points after big corrections always bring significant opportunities for investors. Over the past 50 years an investor buying in at the bottom of a CRE cycle has been handsomely rewarded on a risk adjusted basis.

As the chart below shows – buying ‘low’ (post correction) and riding the upswing has been extremely lucrative over a 5 year time horizon. Historically core unlevered returns on prime CRE assets have consistently exceeded 10% on a 5-year average basis. This level of return with limited downside risk is hard to ignore.

Chart 3 – CRE Returns for Prime Property over Cycles

Based on CBRE Prime Property Indices - calcs from Tristan.

Getting invested has to be the greatest priority for LPs!

Right now, we see some interesting pathways to exploiting the cyclical opportunity across the capital stack with excellent risk adjusted returns on offer across a wide range of credit and equity strategies.

We spent a lot of time over the last 2 years laying out our views on the credit opportunity – we believe it remains an 8-10% returning opportunity (net). Given the returns (which are outsized for CRE credit on an historic basis) and the secular shifts going on in the sector (that will allow non-bank investors to build scale quickly), credit is one of our highest conviction CRE investment themes.

That said, with the cycle now turning the opportunity to earn 10%-20% returns in the equity space is back at front of mind again. As with any new cycle, the equity opportunity will range across the risk spectrum all the way from core to opportunistic. Big cycles always create dislocation, distress and opportunistic investors with lots of risk tolerance are always well positioned to gain immediate and substantial upside benefit, but equally there can also be some interesting (and often overlooked) opportunities for investors with less risk tolerance. One such opportunity is clearly visible right now in core and core+ CRE funds.

Current Core+ opportunities!

Clearly given the equity returns on offer (assuming a normal recovery cycle), being able to buy straight into an existing low risk CRE fund looks compelling. Most specifically, there are a number of high-quality Core and Core+ funds that have exit queues where secondary trades are still possible at modest discounts to net asset value. If you can access a fund with a NAV that fully reflects market prices and there is a small (because NAV is reliable) but meaningful (say 5%) discount, then this is a major opportunity to buy the bottom at a discount to NAV and to get fully allocated or, indeed, to leg-in/cost-average into the opportunity over a couple of quarters.

Points to note before you pull the trigger!

It goes without saying that choice of fund manager, asset base and investment style matters massively when it comes to making an allocation decision. In our view, the best Fund's are always aggressively repositioning into assets and sectors that will maximise the benefits of any upswing and their teams are sweating every asset to maximise operating cashflows to boost performance as the cycle accelerates. We suggest that this best achieved by taking a more active approach, typified in a Core+ style. By the same token, our experience over prior cycles suggests taking some measured Core+ risk at the inception of a cycle tends to pay exceptionally well, as many investors carry their prior cycle PTSD over into the recovery and fail to focus fully on the forward-looking opportunities that arise as the market recovers.

The determination of a rebased NAV is clearly also critical in the execution of any opportunity. Funds that are still focussed on yesterday’s NAV may not be alive to tomorrow’s opportunity and they may struggle to position for it. NAV should be clear and easy to test. In our view a core or core+ fund NAV needs to have been produced consistent with INREV guidelines, with an external appraised independent valuation that would stand the test of audit scrutiny. An NAV should be produced quarterly – not just when it suits the manager. An NAV should reflect market prices and this should be tested with sales and acquisitions. Investors that are thinking about allocating capital need to scrutinise NAV’s so that they can have confidence that their basis is robust, the manager is focussed on the future and thus that their capital is going to be invested wisely to capture the cyclical upside.

The CRE industry is at best inconsistent when it comes to the statement of NAVs. As the chart below from Bloomberg illustrates, some managers have clung onto historic book values that fail to reflect the reality of current market prices. We might want to call them ‘flat-liners’.

Chart 4 – Property Fund NAV’s vs REIT stocks

Flat-lining funds are not solely the preserve of obscure managers. Some very large private markets firms, that should know better, are in this sample. The impacts can be simply summarised:

• Funds who have taken their marks will get the benefit of the cyclical upswing ... but people in the funds with NAVs that have ‘flat-lined’ since 2021 will not so their performance will also be flat going forward. The time weighted effects will begin to bite, so ‘flat-liners’ will underperform on the most relevant relative metrics into a recovery.

• Funds who have taken their marks will receive inflows and may make new investments at better prices and are then also able to reposition more aggressively for new sources of growth ... so their upside can be maximised. ‘Flat-liners will be trapped in yesterday’s portfolios limited flexibility, so their performance will take a further hit.

• Funds who have taken their marks will be able to trade assets at NAV or better and thus offer clear price discovery. This will allow them to raise new capital that should allow them to demonstrate how they will be able to provide liquidity to their existing investors over time, while still growing and adapting their portfolio. LP’s with capital in 'flat-liners' may find that liquidity will be limited and they will be forced to sell high quality assets and shrink their portfolios.

None of this is new news … it happens in every cycle. It creates a distinctive pattern of winners and losers in every recovery cycle. The managers that do the right thing thrive. For most of 2023 people were using the phrase ‘survive til 25’ as a way to paraphrase their approach … well ‘25’ is now less than 4 months away and surviving a down-cycle doesn’t guarantee outperformance on the way up… its time to think forward.

So what?

There is a clear message here. The market is turning. There are significant credit and equity opportunities for CRE investors. Some groundwork is needed to exploit the window of opportunity but that’s no great surprise for CRE veterans. And as we have learnt time and again in prior cycles, waiting for the all-clear to start that work means missing out on the best opportunities. Now is the time to act.